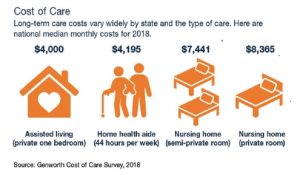

Life Insurance with Long-Term Care Benefits

If you are concerned about the high costs of long-term care but don’t want to purchase traditional long-term care (LTC) insurance, you might consider two strategies that combine permanent life insurance coverage with long-term care benefits.

Keep in mind that any payouts for covered LTC expenses reduce (and are usually limited to) the life insurance death benefit that would go to your heirs, and benefits can be much less than those of a traditional long-term care policy.

Accelerated death benefit (ADB) rider

An ADB rider attached to a permanent life insurance policy allows the insured to begin receiving benefits while he or she is still living, under specific circumstances.

In the past, ADB riders only paid when a policyholder was diagnosed with a terminal illness. However, more insurers now offer riders that start paying when a policyholder is diagnosed with a chronic illness, is permanently disabled, or needs to enter a nursing home.

Although some policies may include an ADB rider at little or no cost, ADB riders are generally optional and will increase the premium.

Hybrid life—LTC policy

This type of policy combines permanent life insurance and long-term care coverage. Many such policies require a substantial up-front premium, but buyers don’t have to worry about future rate increases or the issuer canceling the policy.

For the same premium, a hybrid policy typically has a smaller death benefit than a life policy with an ADB rider. However, the LTC coverage is more generous than an ADB rider.

Benefits under a hybrid policy typically begin when the policyholder needs help with two or more activities of daily living such as eating, bathing, and dressing.

With an optional continuation-of-benefits rider, payouts for covered LTC expenses could continue for a specified period or your lifetime, even if they exceed the death benefit.

Financial flexibility

Another advantage of these strategies is that policyholders can tap into the cash value of the permanent life policy during retirement if money is needed for income or emergencies. Loans and withdrawals will reduce the policy’s cash value and death benefit.

Other considerations

It would be wise to explore your LTC options while you are healthy. If you consider a a life insurance policy with an ADB rider or a hybrid life-LTC policy, you should have a need for life insurance and evaluate the policy on its merits as life insurance.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. In addition to the life insurance premiums, other costs include mortality and expense charges. If a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Any guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company. Riders are subject to the contractual terms, conditions, and limitations outlined in the policy, and may not benefit all individuals.