The Level of Corporate Debt is Troubling

The amount of corporate debt has recently reached $1 trillion. Research from Bloomberg News firm found that businesses have taken advantage of over a decade of low interest rates to make acquisitions – substantially increasing their debt load.

Looking at a few of the acquisitions, the investigators found that companies commonly borrowed two to six times their annual earnings. This level of debt suggests these companies may struggle to pay their bondholders back – particularly if a more severe recession should occur. Surprisingly, we have not seen many debt downgrades by the rating agencies.

A good illustration is Campbell Soup Company, who borrowed over $6 billion to purchase Snyder’s-Lance Inc. (they make the type of snacks you purchase in vending machines). Campbell Soup now has more than $10 billion in debt – more than 5 times its earnings before taxation, interest, depreciation and amortization –a metric known as EBITDA.

What did the bond rating agencies do? Not much. Campbell Soup is still rated as investment grade as the rating agencies expect the merged company to generate enough revenue (and reduce costs) to quickly pay down the debt. Perhaps so. But actual results have a funny way of being different than projected results.

Additional instances include: Dr. Pepper Snapple Group quadrupled its debt burden when it bought Keurig Green Mountain Inc. at a $18.7 billion deal. Its debt is now 5.6 times EBITDA. AT&T took on additional $190 billion to finances the purchases of DirecTV and Time Warner. Bayer bought Monsanto for $63 billion, increasing its debt far beyond the levels of a typical investment grade company. Overall, Bloomberg identified 50 cases where companies took on enough debt to normally lower their ratings to junk status. Yet, they kept their investment grade rating.

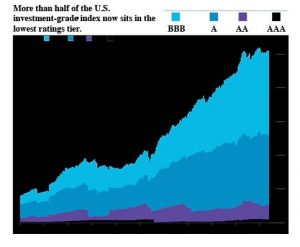

The chart on the following page shows that more than half of corporate bonds are rated BBB or A – just one or two notches above junk bond status. When the next recession hits (who knows when but there will bill one), we would expect to see a higher level of corporate bond downgrades, and maybe even more defaults. Perhaps one of the unintended consequences of the decades long low interest rate environment.